Food and Beverage Industry Trends Are Reshaping Economic Development

The food and beverage industry continues to be a major driver of economic activity across the United States. As consumer preferences evolve, supply chains shift, and companies face rising cost pressures, economic developers must stay closely attuned to both structural and cyclical changes affecting the sector.

This article explores key trends shaping the food and beverage industry, including how activity and specialization vary across regions of the country. It also highlights four critical factors influencing market conditions and redefining the role of economic developers. These insights are informed by national labor market data as well as feedback Camoin Associates is hearing directly from food and beverage executives actively evaluating expansions and relocations through the lead generation process.

Understanding how existing companies are navigating these challenges — and where new opportunities are emerging — will be critical for communities looking to retain their current business mix and guide strategic investments in line with shifting market dynamics.

Recent Food and Beverage Industry Conditions

Over the last decade, labor market data indicate that the food and beverage industry has experienced strong growth. Employment increased by 23 percent, while Gross Regional Product (GRP) expanded by 44 percent. Notably, this pace of job growth outperformed the overall U.S. economy, which grew by approximately 11 percent over the same period.

Key drivers of employment growth include subsectors such as beverage manufacturing and animal food manufacturing.

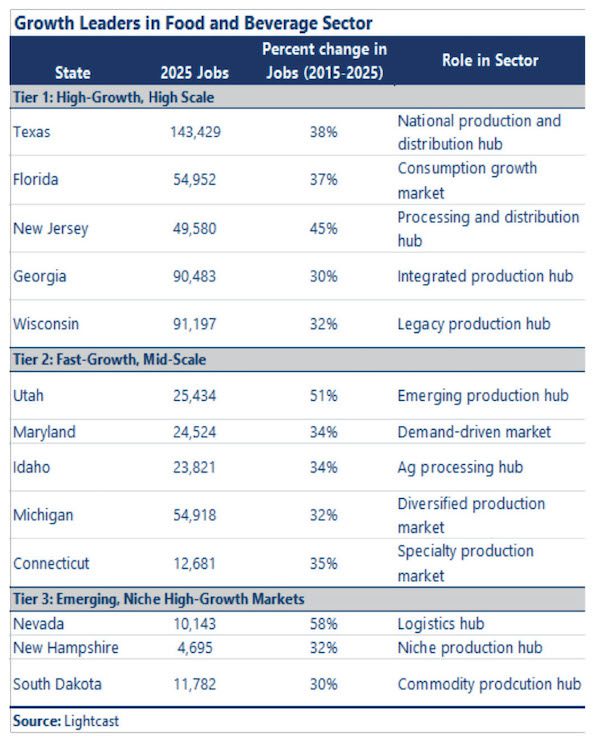

Across the country, regional dynamics vary significantly, with different areas specializing in distinct segments of the industry. States such as Texas, Florida, and Georgia remain dominant agriculture hubs, while Midwestern states like Wisconsin continue to serve as legacy production centers.

At the same time, several mid-sized and emerging markets are gaining traction. Utah has emerged as a fast-growing production hub, Michigan benefits from a diversified manufacturing base, and Connecticut is carving out a niche in specialty food production within the Northeast. Smaller markets, including New Hampshire and South Dakota, have also seen notable growth over the past decade.

Spotlight on Sioux City and Sioux Falls

The Sioux City MSA, spanning Iowa, Nebraska, and South Dakota, stands out for both its growth and industry concentration. The region’s strength is driven by animal slaughtering, meat processing, and pet food manufacturing, making it one of the nation’s most concentrated food processing hubs.

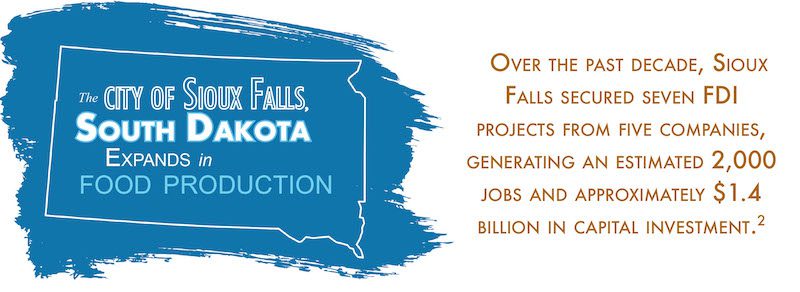

Foreign direct investment trends further highlight the region’s momentum. Sioux Falls, South Dakota, has attracted notable investment activity, ranking alongside much larger markets such as St. Louis, Houston, and Los Angeles.

Over the past decade, Sioux Falls secured seven foreign direct investment projects from five companies, generating an estimated 2,000 jobs and approximately $1.4 billion in capital investment.

This growth trajectory continues into 2026. In February, Smithfield Foods, Inc. announced plans to construct a state-of-the-art packaged meats and fresh pork processing facility in Sioux Falls. Located within the 1,000-acre Foundation Park development, the new facility will replace the company’s existing plant and is described by the company as “among the most modern of its kind in the United States.”

Key Takeaways Shaping the Food and Beverage Industry

While a wide range of forces are shaping investment in the food and beverage industry, four key dynamics have an outsized impact on market conditions. These factors also influence how economic developers can position their communities for new investment.

1. Demand Is Stable, but the Product Mix Is Rapidly Evolving

Consumers are increasingly gravitating toward health-focused foods, functional foods, and premium offerings that align with lifestyle and wellness goals. This shift has contributed to market share losses for traditional categories such as traditional sodas, white bread, and mainstream beer.

Growth is concentrating in value-added segments where companies can command higher margins through product differentiation and distinctive branding.

This shift is also influencing product form and distribution. The continued rise of “snackification” — products designed in smaller portions, grab-and-go formats, or convenience-oriented packaging — reflects changing eating habits among consumers who are constantly on the go.

For producers, these trends are driving demand for new processing techniques and packaging formats.

What Camoin Associates Is Hearing from Executives

Many companies have recently emphasized that future growth will not come from volume alone, but from processing sophistication and brand-aligned production.

Executives consistently point to the need for facilities that can support flexibility for product line changes, specialty SKUs, and innovative packaging rather than single, legacy products.

2. Mounting Margin Pressure Is Driving Operational Decisions

Despite steady demand, profitability across much of the industry remains constrained. Many subsectors operate on thin margins, typically ranging from two to eight percent, making cost control a central driver of location and investment decisions.

Input volatility is a major factor. Agricultural inputs such as grains, dairy, and sugar have experienced significant price swings, compounded by rising fertilizer costs and ongoing geopolitical instability.

In addition to raw materials, companies face persistent pressure from labor costs, shifting immigration guidelines, and regulatory compliance.

What Camoin Associates Is Hearing from Executives

Margin pressure is shaping nearly every site decision. Executives consistently cite labor availability, logistics efficiency, and existing building readiness as more important than incentive value alone.

In particular, companies prefer existing food-grade facilities that reduce upfront capital costs and accelerate speed to market.

3. Global Competition and Trade Dynamics Are Reshaping Supply Chains

Globalization continues to play a defining role in the food and beverage sector, with American producers competing with importers for specialized and globally inspired products.

Imports are prevalent in segments such as seafood and specialty ingredients, often due to limitations in what the United States can produce based on climate or perceived authenticity. Domestic producers also face price competition from lower-cost international suppliers, especially in labor-intensive segments.

At the same time, trade policy uncertainty and tariffs introduce volatility, particularly for perishable imports.

What Camoin Associates Is Hearing from Executives

Canadian manufacturers are particularly interested in siting additional operations in the U.S.

Camoin Associates has had conversations with several Canadian companies evaluating U.S. manufacturing or distribution entry on compressed timelines, driven by trade policy uncertainty. In many cases, these companies are expanding into the U.S. to serve U.S. consumers from U.S. facilities, not to export.

4. Technology Is Redefining Production, Distribution, and the Consumer Interface

Technology adoption is accelerating across the food and beverage sector, not only in production but across the entire value chain.

AI-driven supply chain management and smart packaging are becoming standard tools for managing costs and responding to changing consumer expectations. These digital tools are a direct response to margin pressures and the need for speed, flexibility, and operational efficiency.

What Camoin Associates Is Hearing from Executives

Companies increasingly expect communities to support technology-enabled operations, whether through workforce pipelines, utility capacity, or zoning that accommodates advanced processing and cold-chain infrastructure.

Real-World Implications: The Dairy Industry as a Case Study

A recent analysis of the New England dairy sector for the Northeast Dairy Business Innovation Center offers a real-time case study of how broader food and beverage trends are reshaping the industry.

The takeaway is clear: this is less about decline and more about a fundamental shift in where value is created.

Dairy faces the same pressures seen across the industry, including tight margins and a rapidly changing product mix. Traditional fluid milk operates on thin margins, contributing to the loss of smaller farms. At the same time, remaining operations are becoming larger and more productive, reflecting a shift toward scale and efficiency.

Growth is increasingly concentrated in value-added and specialty products such as cheese, yogurt, and organic dairy products, which offer stronger margins and better alignment with consumer preferences.

In New England, this has helped stabilize processing activity even as farm-level production declines.

What Food and Beverage Trends Mean for Economic Developers

If your community has strengths in any segment of the food and beverage sector, these trends point to a clear set of priorities for remaining competitive in attracting and retaining investment.

The communities best positioned to capture this activity are those focused on real estate readiness, speed, infrastructure, and targeted outreach.

Prioritize Food-Grade Real Estate Readiness

Demand for existing or conversion-ready FDA- and USDA-compliant facilities far outpaces supply. Communities that can identify and accelerate access to these assets offer a decisive advantage.

Based on conversations with business executives, site readiness often outweighs incentive value alone.

Compete on Speed and Flexibility

With margins under pressure, factors such as speed-to-market, operational flexibility, and reduced upfront capital costs are valuable assets for companies.

Programs and processes that shorten permitting timelines or support workforce onboarding can directly influence location decisions.

Align Infrastructure with Advanced Processing Capabilities

Modern food production facilities require robust infrastructure, particularly reliable water and energy capacity to support cold-chain logistics and technology-enabled operations.

Economic developers who can collaborate with utility providers and local jurisdictions to address complex or persistent infrastructure challenges will be viewed as competitive partners.

Target Market-Driven Investment Opportunities

Growth is increasingly driven by serving U.S. consumers from domestic facilities, including near-term interest from Canadian companies responding to trade uncertainty.

Outreach efforts should highlight a community’s logistics advantages and proximity to key customer markets. Showcasing the presence of reliable suppliers that support ongoing operations will also stand out in the business location decision-making process.

About the Authors

Alex Tranmer is Director of Industry and Workforce at Camoin Associates. As a Senior Project Manager, Alex leads complex strategic planning efforts in geographies ranging from bustling urban centers to pastoral villages. She harnessed the power of collaboration in Los Angeles County, the country’s most populous county, where she managed a multi-disciplinary team to develop a strategic plan that was swiftly approved by the U.S. Economic Development Administration. Alex works with clients to balance the competing interests of stakeholders while helping them develop plans that are ambitious yet achievable under their existing organizational capacity.

Tori Conroy is a Senior Project Manager at Camoin Associates. Tori is passionate about finding solutions to complex problems by being creative, collaborative, and engaging diverse stakeholders. She has a background in public administration, economic development, and marketing. Prior to working for Camoin Associates, Tori managed and worked with three different economic development authorities and enjoys strategic and organizational planning.

Bridget Byrnes is an Analyst at Camoin Associates. Bridget brings a unique perspective in economic research, data analysis, and community-focused work, supported by a master’s degree in public administration with a concentration in economic development. Her background has honed her ability to communicate effectively, translate complex information for diverse audiences, and manage projects with precision and care.

Sources

- Labor market data drawn from Lightcast

- fDi Markets, Trends Report FDI Food and Bev, January 2015–December 2025

- Greater Sioux Falls Chamber of Commerce, Smithfield Announces Plans for New Sioux Falls Facility, February 24, 2026

- IBISWorld

- IBISWorld

- PBS News, Farmers warn of food price spike as war drives up fuel and fertilizer costs, April 6, 2026

- IBISWorld